The Indian IT industry has lost roughly $50 billion in market value amid rapid advancements in AI, particularly following recent major updates to coding systems like Claude and other AI development tools. This has created serious concerns over the future of Indian listed IT stocks and whether they can even sustain in an environment where AI is increasingly capable of doing what thousands of developers were once hired to do.

For this research we’ll take the top five Indian listed IT companies on the basis of market cap as a reference point: Tata Consultancy Services, Infosys, HCL Technologies, Wipro, and LTIMindtree.

Now, when you visit their websites, it’s the same script everywhere. AI. Data. Digital transformation. Intelligent automation. AI powered enterprises. Yada yada. Everyone claims to be leveraging AI at scale. If that is the case, then what exactly is the problem?

The Current Business Model & The Problem

To understand that, we need to understand what business these companies are really in. Broadly, they operate in two models. One is IT services, where they provide consulting, development, integration, maintenance, outsourcing. The second is IT products and platforms, where they offer proprietary solutions and domain-specific software.

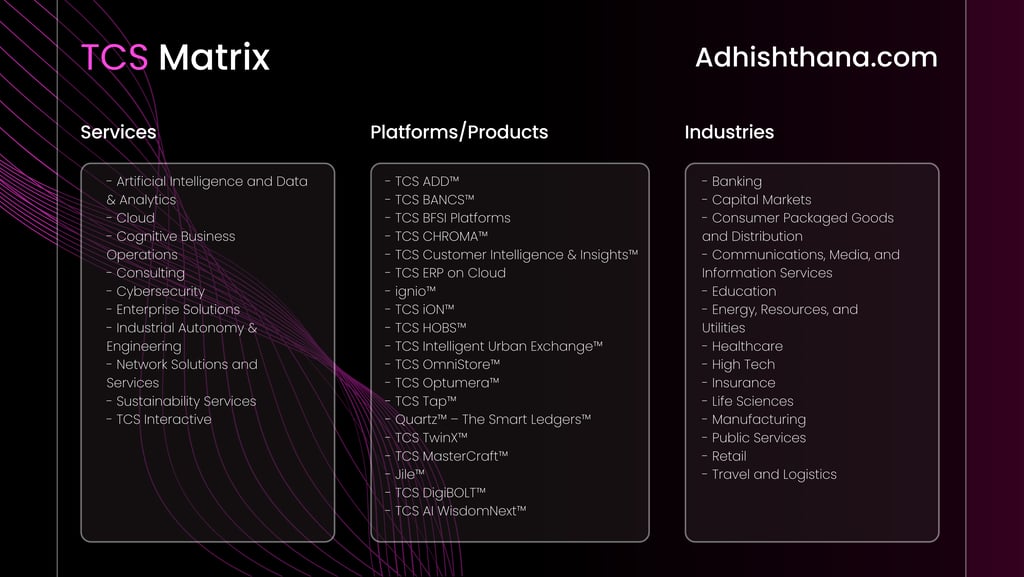

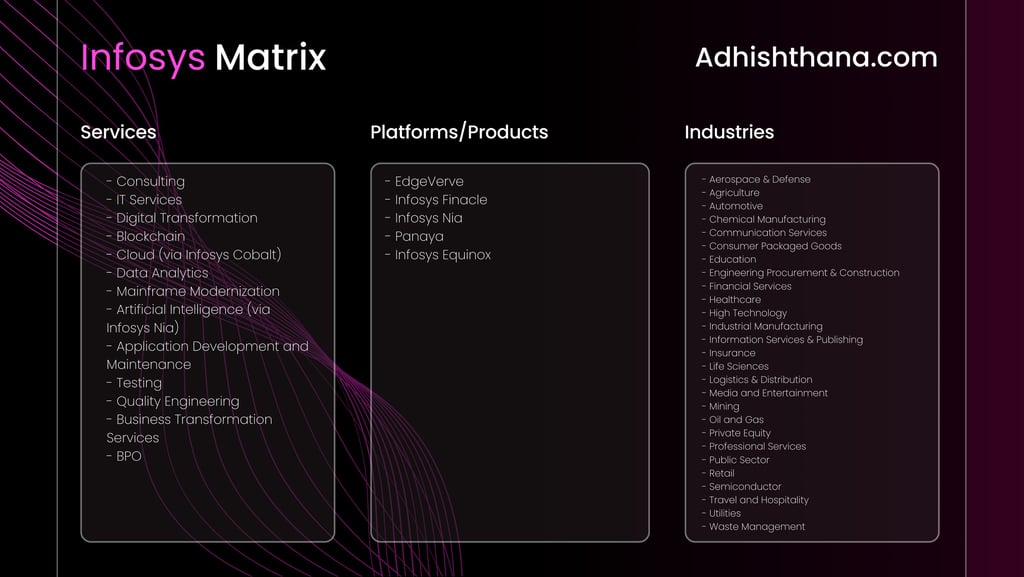

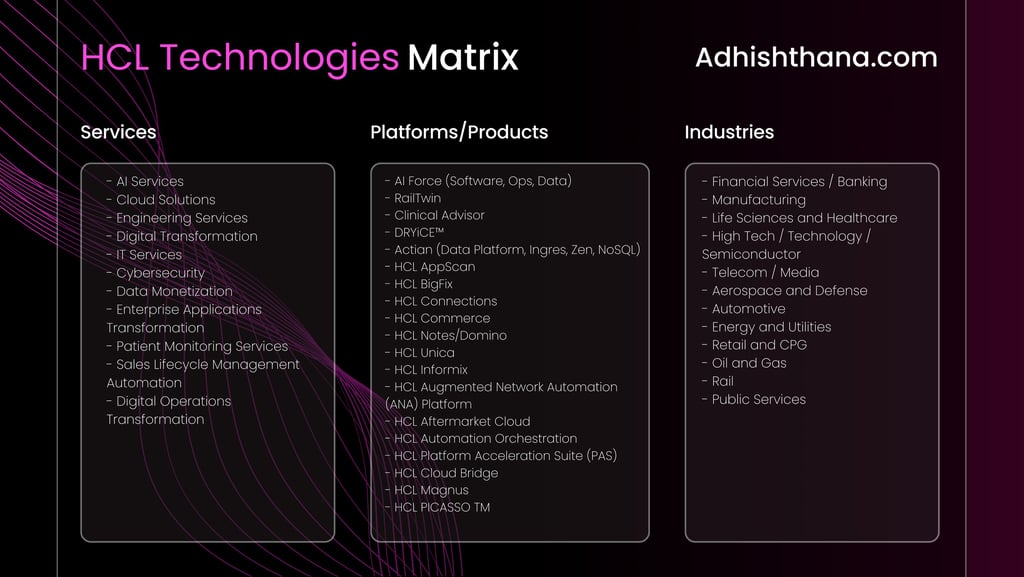

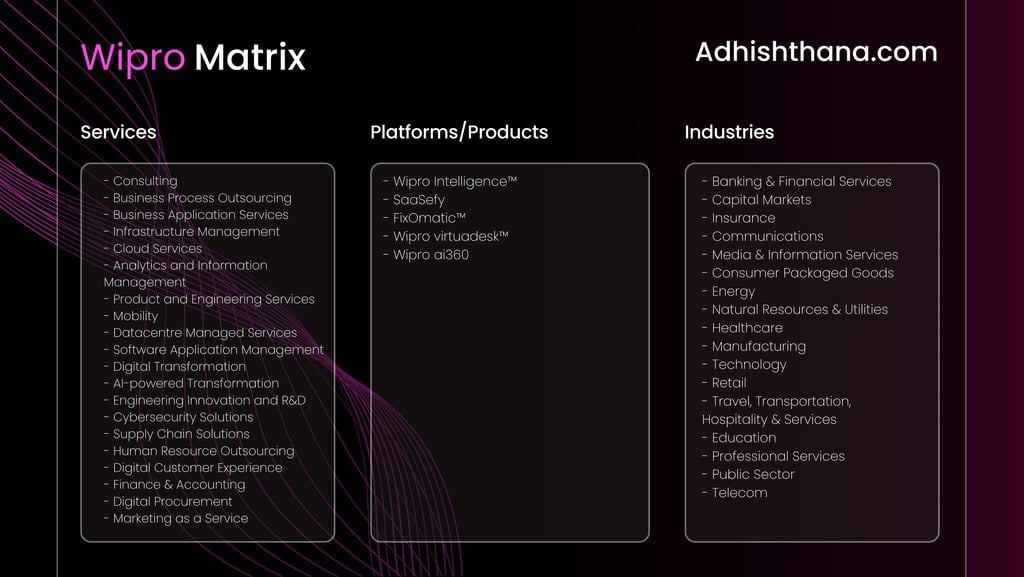

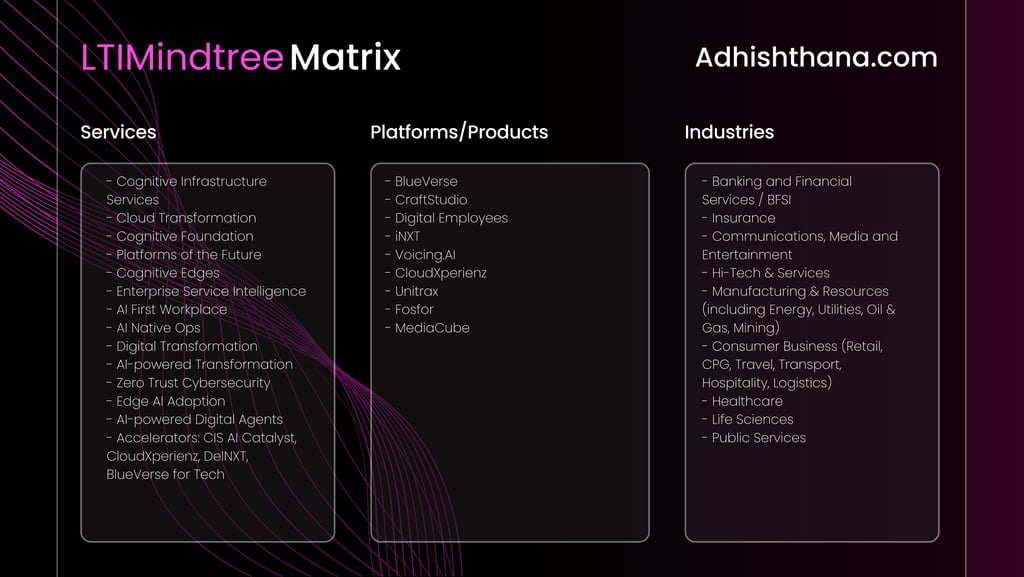

In the tables below, we outline the services these companies provide, the platforms and products they offer, and the domains they operate in, so you have a detailed understanding of the breadth and structure of their businesses.

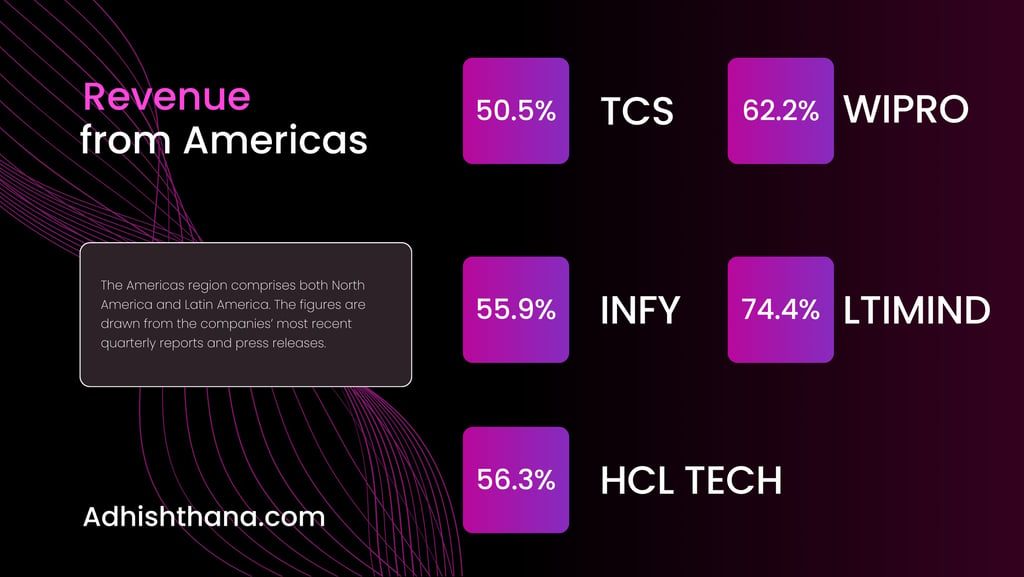

The uncomfortable truth is that the majority of revenue across all these companies still comes from the services side. Not products. And geographically, the biggest consumer of these services is the Americas.

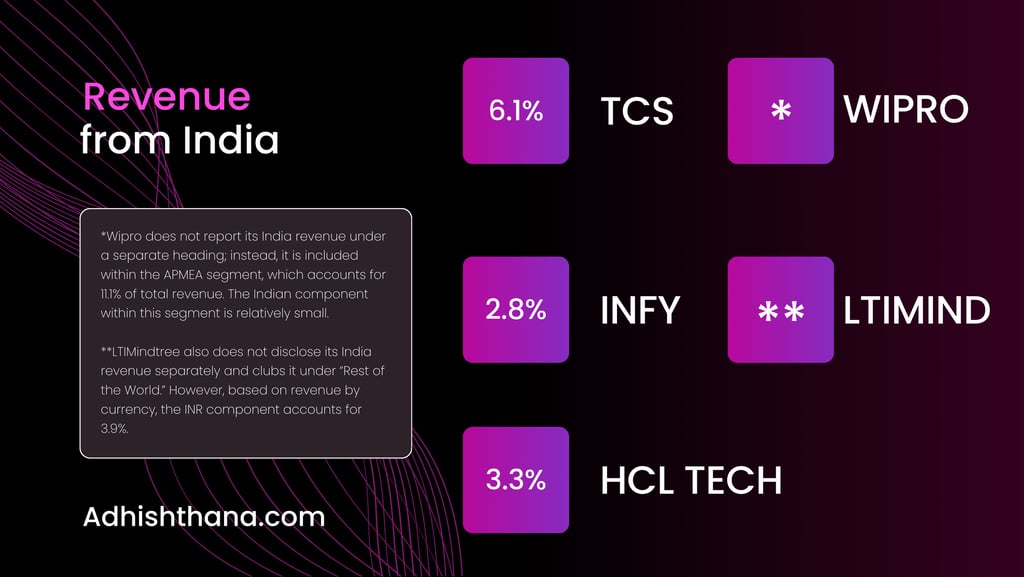

In the tables below, we summarize the revenue these companies derive from the Americas versus Indian clients. In several cases, the revenue contribution from India is so minimal that it is either clubbed under “Rest of the World” or grouped within broader regions such as APMEA, highlighting how small the domestic component actually is.

There is nothing inherently wrong with that model. It built massive wealth and created millions of jobs. But that model was designed for a different technological era, one where software development was manpower intensive and required large distributed teams. That assumption is now being challenged by AI.

With the rise of coding systems from Anthropic, OpenAI, Google DeepMind, xAI and tools like Cursor, the economics of building software is changing fast. These systems can write production-level code, refactor it, test it, generate documentation and significantly reduce development cycles. If you are a global enterprise with an internal tech team, your dependency on large outsourced coding teams reduces. Not because you don’t need software, but because you need fewer people to build it.

With the rise of coding systems from Anthropic, OpenAI, Google DeepMind, xAI and tools like Cursor, the economics of building software is changing fast. These systems can write production-level code, refactor it, test it, generate documentation and significantly reduce development cycles. If you are a global enterprise with an internal tech team, your dependency on large outsourced coding teams reduces. Not because you don’t need software, but because you need fewer people to build it.

For example earlier, let’s assume a US-based pharma company that wanted to build a prescription management system would outsource the entire project to an Indian IT giant instead of hiring expensive local developers. The Indian company would deploy developers (let’s say 10 for this example), understand requirements, build the system, coordinate with the client’s internal tech team, and bill for manpower and time.

Note: There is also a huge sub-outsourcing layer in India where the large IT company would win the contract at a higher rate and outsource part of it at a lower rate, capturing the margin difference. The model worked because development was slow, teams were large, and execution required human effort at scale.

Now imagine the same pharma company today. Their senior developers use AI tools internally to generate code. Prototypes are built faster. Iterations happen quickly. Instead of needing ten external developers, they might need two specialists to review, test and ensure compliance. As AI models improve further, even that number reduces. The demand shifts from bulk coding manpower to high-skill architects and reviewers. That shift is structural, not cyclical.

This is where Indian IT faces trouble. These companies have massive workforces built for scale. Their margins depend on utilization. If clients reduce team sizes, billing hours fall. Utilization drops. Hiring slows. Layoffs begin. The entire services-heavy revenue model comes under pressure. The global IT services pie is not disappearing overnight, but it is becoming more automated and more concentrated around high skill talent rather than large execution teams.

Adhishthana Analysis

Now let’s examine these stocks through the lens of the Adhishthana principles. We will first track their respective phases on the Indian listed equities and then analyze their ADRs to gain clearer structural confirmation.

This paints a troubling picture. Infosys and Wipro, on the monthly structure, have broken their Cakra pattern, triggering the Move of Pralaya.

As I outlined in Adhishthana: The Principles That Govern Wealth, Time & Tragedy:

“When the underlying breaks the Cakra on the flip side, consolidation typically extends into the Guna triads. The move that follows is highly significant, and selling pressure can be extremely strong. This is called the Move of Pralaya.”

Structurally, that implies prolonged weakness.

HCL Tech appears to be inching toward a similar breakdown. TCS, being in Phase 6, does not show a confirmed structural collapse yet, but retrospectively it has shown one of the weakest alignment with the Adhishthana principles, which is not a comforting sign. LTIMindtree had rallied prematurely during its Buddhi phase, something that ideally should not have happened at that stage, and the current correction is structurally valid within that framework.

As for the Adhishthana monthly phases of the ADRs, only Infosys and Wipro have actively traded ADRs available for analysis, and in both cases the structure broadly echoes the Indian listings. For Infosys, the ADR is currently in Phase 8 rather than Phase 9 as seen in the Indian market, but it has already broken the Cakra within this phase, reinforcing the prevailing bearish structure. The weakness in the Indian chart is clearly reflecting in the ADR as well. In the case of Wipro, the ADR is in Phase 7 and has also broken its Cakra, pointing toward a similar downside risk. US investors holding these ADRs should remain cautious given the structural breakdown visible on both sides.

All in all, the Indian IT giants are placed in a bearish structural alignment as per the Adhishthana model. Interestingly, the fundamental story and the structural positioning are pointing in the same direction. Investors are asking a simple question. Why allocate capital to service-heavy businesses facing margin compression when there are companies with proprietary chips, semiconductors and product-backed tech with stronger structural moats?

What is the way ahead?

So are these companies dead? No. But they cannot remain what they were if they continue the way they have been managing their business so far. The only sustainable path forward is product-led transformation. The consultation services vertical cannot be the primary growth engine forever. Their proprietary platforms and domain products are the only parts that can create defensible long-term value. The company that builds scalable, AI-native enterprise products will have the edge.

Investors already understand this. The majority of revenue still comes from services, and services are facing structural compression. That is why valuations are resetting. Markets are pricing slower growth, margin pressure, and transition risk. Until product revenues become meaningful and visible, the overhang will remain.

In the short term, smaller companies and subcontractors might benefit as clients try to cut costs and bypass large IT majors. But even that is temporary. Coding AI compresses value chains everywhere. In the long run, the only defensible roles are deep domain experts, system architects, AI governance specialists and senior engineers who truly understand what the AI is producing. Bulk coding roles are vulnerable.

The Indian IT export story was built on labor arbitrage and scale. AI challenges both at the same time. This does not automatically mean collapse, but it does mean transition. The next decade will determine whether Indian IT giants transform into AI-native product companies with proprietary technology, or remain legacy service exporters in a world that needs fewer coding armies. That is the real question. So what is the way forward?

The answer cannot be more services. The only defensible path is products. Proprietary platforms. Domain specific AI native systems.

From the tables we shared earlier, it is clear that among the large players, Tata Consultancy Services arguably has one of the broader proprietary platform portfolios. That gives it relative strength. But they cannot just rely on legacy platforms and incremental upgrades. They need to aggressively expand into proprietary AI layers, domain specific models, and infrastructure ownership.

TCS recently announced initiatives like HyperVault, its own data center infrastructure play. That direction is critical. In an AI driven world, whoever controls data, compute, and enterprise platforms controls the value chain. If Indian IT giants remain dependent on third party infrastructure and third party intelligence, they will always sit one layer below the real value creation. Owning data centers, building secure enterprise AI environments, and creating proprietary model wrappers around enterprise data is not optional anymore. It is foundational.

Alongside infrastructure, deep partnerships with global AI leaders will be essential. Not superficial marketing tie ups, but real integration. Collaborations with companies like Anthropic, OpenAI, Google DeepMind and xAI must translate into enterprise grade AI solutions. Similar to how Infosys’s recent strategic partnership with Anthropic integrates Claude models and Claude Code into its Topaz AI platform to build industry specific AI agents. The opportunity is not in reselling AI access. It is in embedding AI into industry specific systems at scale.

And then comes structural boldness. In my opinion, TCS should seriously consider consolidating technology focused group entities like Tata Technologies and Tata Elxsi into a single integrated technology powerhouse. Instead of fragmented capabilities across listed entities, a consolidated platform driven AI native technology conglomerate could create scale, deeper R and D alignment, and stronger intellectual property positioning (especially for their own products like self driving technology for Tata vehicles, similar to how Tesla AI is building and integrating autonomous systems within its own ecosystem). In the current environment, incremental change will not be enough. Structural boldness is required from the leadership.

But all of this is forward looking. Today, the numbers still show that the majority of revenue comes from IT services, and that segment is structurally compressing. Investors know this. A valuation reset is already underway. Stocks that have triggered the move of Pralaya under the Adhishthana framework are likely to face prolonged consolidation and underperformance in both the Indian markets and the US ADRs, unless there is visible evidence of product-led transformation.

In the short term, smaller companies may benefit as clients bypass large IT majors and chase lower costs. But that too is temporary. AI compresses margins across the entire chain. The only durable value will sit with companies that own proprietary platforms, proprietary intelligence, and senior talent capable of governing AI driven systems.

The Indian IT export story was built on labor arbitrage and scale. The next chapter will be built on ownership of intelligence, infrastructure and intellectual property. The companies that understand this and move decisively will survive the transition. The ones that hesitate will slowly become legacy service providers in an AI first world.

Contact

business@adhishthana.com

shivank@adhishthana.com

© 2026 Adhishthana. All rights reserved.